Venture-backed private companies maintain executive compensation programs that are significantly different than public company programs. This does not mean a venture-backed private company that is planning an initial public offering needs to immediately make drastic changes to its programs to conform to public company practices, proxy advisory concerns and regulatory issues. However, Compensation Committees of these companies should consider transitioning their programs and practices over a three-year period starting prior to the IPO and continuing for several years following the IPO. This pre-IPO checklist provides a roadmap to help Compensation Committees and management teams successfully transition their executive compensation programs over time.

A compensation philosophy serves as the foundation for all compensation decision-making including:

Although still not common among public company practices, the Board of Directors should also discuss their preferred approach to the design and amount of Board pay through a philosophy statement.

Just Released: Chief Executive’s 2019-20 CEO & Senior Executive Compensation Report for Private Companies. With data from over 1,600 private companies, it is the most authoritative resource in the U.S. for private company executive pay. Know more, pay smarter. Learn more.

Just Released: Chief Executive’s 2019-20 CEO & Senior Executive Compensation Report for Private Companies. With data from over 1,600 private companies, it is the most authoritative resource in the U.S. for private company executive pay. Know more, pay smarter. Learn more.Disclosing executive compensation practices and decisions and managing to a compensation philosophy is important since the approach a company takes must be disclosed in the Compensation Discussion & Analysis (CD&A) section of the public company’s proxy statement. As a public company, the compensation philosophy disclosure does not need to be detailed, but it needs to accurately reflect how the Compensation Committee manages executive pay.

It is not unusual for a private company to prepare competitive pay analyses on an as-needed basis to address current issues and understand market practices. These analyses are generally not prepared annually and may not be based on public company practices. Most public companies, in contrast, review the total pay levels of their senior leadership team annually with direct comparisons to public company practices driven by CD&A disclosure needs and Say-on-Pay votes. The approach to constructing a public company peer group is an important step in ensuring the Compensation Committee understands public company practices and should follow these generally accepted practices:

relative performance metrics. If the majority of peers do not have similar business models then performance comparisons will be distorted.)

Developing a public company peer group was once thought of as a simple exercise but peer group construction is one of the most important steps in establishing an executive compensation program. Poorly constructed peer groups have been blamed for excessive compensation levels as they are often one of the foundation stones that go into the construction and design of executive pay programs.

Further, with the increased use of relative performance measures, it is critical that the business models and cycles of the peers are aligned with the company. Without this alignment, performance comparisons and awards paid under incentive plans may not truly reflect a company’s relative performance, resulting in incentive awards to executives that are either too small or too generous. For example, if the majority of peers have business models that are not as profitable as the subject company, then awards based on a relative comparison of profitability will result in inflated incentive awards.

Many private companies that are managing to an exit event set aside 8% to 15% of shares for management. Most of these shares are typically granted to the management team in a single equity grant, while the remaining shares are set aside for future grants to existing and new hires. In many cases, members of the management team may not receive a subsequent equity grant until the IPO. Assuming the cash compensation levels (salary plus bonus) are competitive, Compensation Committees have been comfortable that setting aside 8% to 15% of equity for management will result in fully competitive total pay levels, especially given the expectations of high equity returns upon a successful IPO exit.

In the past, it was not unusual for a private company to expect to have an exit event in a three-to-four-year time frame. In today’s economy, particularly since the financial crisis of 2008, it is not unusual for a private company to have an exit event in eight or more years. The amount of time currently needed for an IPO event results in private companies using substantially less equity than a public company over a similar time period.

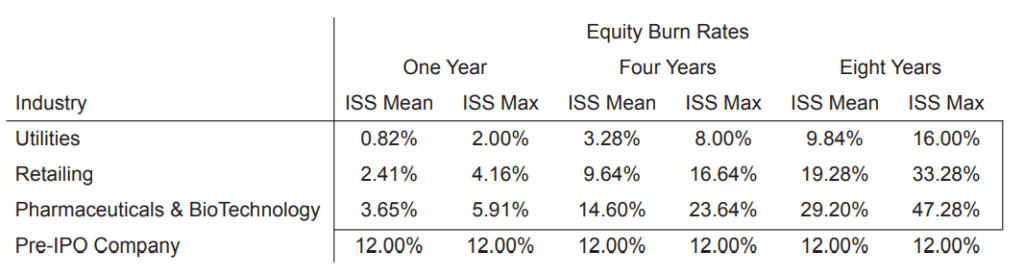

The following table illustrates this concept. Assume a private company issues 12% of outstanding shares to management. Contrast this to the amount of shares that could be granted to management of public companies. For purposes of this illustration, we show the mean and maximum amount of shares that could be granted to employees and Directors of public companies based on current Institutional Shareholder Services (ISS) guidelines. We also selected three industries for this comparison. These industries run the spectrum of low, medium and high users of equity.

We are showing a pre-IPO company that uses 12% of outstanding shares under all scenarios. The chart shows that over a four year period, the private company equity practices are reasonably competitive with public company practices but over an eight year period, private company equity practices become uncompetitive even when compared to industries that are traditionally modest users of equity. Under the latter result, a private company may experience attraction and retention issues as other opportunities may become more attractive.

We are showing a pre-IPO company that uses 12% of outstanding shares under all scenarios. The chart shows that over a four year period, the private company equity practices are reasonably competitive with public company practices but over an eight year period, private company equity practices become uncompetitive even when compared to industries that are traditionally modest users of equity. Under the latter result, a private company may experience attraction and retention issues as other opportunities may become more attractive.

The type of equity granted at private companies differs from public company practices as well. Private companies rely heavily on time-vested restricted stock and stock options and, in many cases, performance-vested options. This type of program is much different from public company practices where the vast majority of equity programs include two to three equity vehicles and where performance-vested stock options are highly uncommon.

The design of the long-term incentive (LTI) plan is one element of the executive compensation program that will need immediate study for a few reasons:

There is abundant market data on long-term incentive plan prevalence and practices, best practice perspectives and summaries of proxy advisory policies on long-term incentive designs. The Committee and management team have access to the information needed to design a long-term incentive plan that will align with public company practices, be motivational and support shareholder growth objectives.

The Board of Director pay practices of a privately-held company differ substantially from public company practices in several ways. In general, venture-backed private company Boards typically include individuals who are employees of the major investors and they may or may not be paid as a Board member. The Board may also include executives with substantial operating experience, financial expertise or other high-level management skills needed at the Board level. These are always paid positions.

For private companies, the Board pay mix will be heavily weighted with equity while cash compensation will be modest when compared to public company practices. The chart below illustrates the differences. This chart compares median Board pay at private companies with $25M to $50M in revenue to public companies with revenues ranging between $50M to $500M. The public company data includes larger companies to illustrate how Board pay will need to change over time once a company becomes public and grows.

This data shows how varied Board pay practices can be in private companies vs. public companies. At private companies, cash compensation may be less than half of public company practices. However, the value of equity may be many times more valuable. In addition, private companies typically do not grant equity each year which is a common practice at public companies.

This data shows how varied Board pay practices can be in private companies vs. public companies. At private companies, cash compensation may be less than half of public company practices. However, the value of equity may be many times more valuable. In addition, private companies typically do not grant equity each year which is a common practice at public companies.

Board pay is a topic that should be reviewed before a company goes public, especially as Board members, who represent the major institutional investors, rotate off the Board. The company will need to maintain a Board pay program that is attractive to new Directors and it will need to be fully competitive as companies vie for talent in this arena.

Private company Compensation Committees have much less concern than do public companies about proxy advisory firm policies on compensation. Additionally, public company pay practices may simply not be important to private company Compensation Committees. Therefore, it is likely a private company will have pay practices that are not common in public company practices and/or may not be aligned with proxy advisory policies. Because of the influence of advisory firms, it is always important to audit a private company’s executive compensation program to understand how it differs from public company practices and to understand if any changes need to be made over time. For example:

Many aspects of executive and Board compensation differ when contrasting public and private company practices. As private companies near an IPO, they should consider conducting an audit of all elements of their pay practices to understand what has to change, what may need to change, and over what period of time. It is important for Compensation Committees to understand that pay programs can evolve over a two- to three-year period post-IPO, which gives the Committee enough time, with careful planning, to seamlessly evolve the program from private company practices to the best practices of public companies.

0

1:00 - 5:00 pm

2:00 - 5:00 pm

10:30 - 5:00 pm

General’s Retreat at Hermitage Golf Course

Sponsored by UBS